The Social Security program pays monthly cash benefits to retired or disabled workers and their family members and to the family members of deceased workers. The Old-Age, Survivors, and Disability Insurance (OASDI) program consists of two parts. Retired workers, their families, and survivors of deceased workers receive monthly benefits under Old-Age and Survivors Insurance (OASI) program. Disabled workers and their families received monthly benefits under the Disability (DI) program.

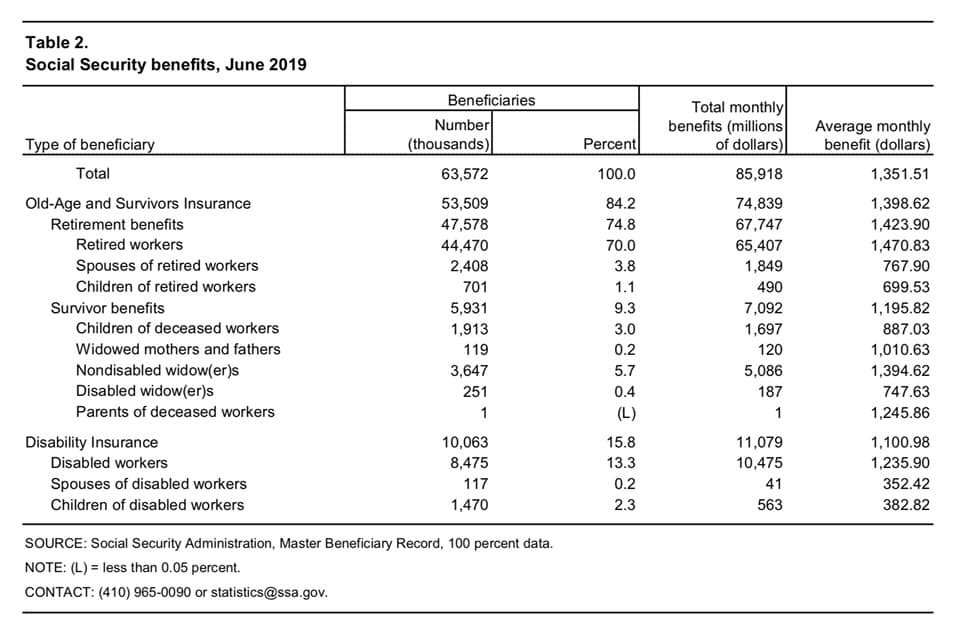

According to the most recently released “Snapshot” from the Social Security Administration (SSA), 63.57 million people received payments, segmented as follows:

Additionally, each year the SSA releases a Trustees report outlining important actuarial statistics assessing the financial health of the OASDI programs. The last eight Trustees reports have indicated that the OASDI Trust Fund reserves would become depleted between 2033 and 2035 under the immediate set of assumption. The 2019 Report from the Trustees contains the following warning:

“Under the intermediate assumptions, the projected hypothetical combined OASI and DI Trust Fund asset reserves become depleted and unable to pay scheduled benefits in full on a timely basis in 2035. At the time of depletion of these combined reserves, continuing income to the combined trust funds would be sufficient to pay 80 percent of scheduled benefits. The OASI Trust Fund reserves are projected to become depleted in 2034, at which time OASI income would be sufficient to pay 77 percent of OASI scheduled benefits. DI Trust Fund asset reserves are projected to become depleted in 2052, at which time continuing income to the DI Trust Fund would be sufficient to pay 91 percent of DI scheduled benefits.“

The depletion in 2035 is driven by the retirement of the baby-boom generation, who will increase the number of beneficiaries much faster than previous lower birth rate generations can offset. The Trustees predict this phenomenon will cease between 2040 and 2051, when “the aging baby-boom generation is gradually replaced at retirement ages by subsequent lower-birth rate generations.

In 2015, the Trustees predicted that the DI trust fund would run out of money at the end of 2016, but Congress passed H.R. 1314 “Bipartisan Budget Act of 2015,” which temporarily changed the percentage tax rate of money going into this fund. As a result of the boost in funding and a declining number of disability applications since 2010, the solvency date changed to 2052. P.L. 114-74 § 833 codified an adjustment of the income tax rate from 1.80% to 2.37% until January 1, 2019.

Considered separately, the OASI Trust Fund reserves become depleted in 2034 and the DI Trust Fund reserves become depleted in 2052. In last year’s report, the projected reserve depletion years were 2034 for OASDI, 2034 for OASI, and 2032 for DI. The report calls for legislation action, but warns that in the “absence of such legislation, continuing income to the trust funds at the time of reserve depletion would be sufficient to pay 77 percent of OASI benefits and 91 percent of DI benefits.

The legislative proposals will be evaluated in an subsequent analysis.

Additional Reading:

Social Security: Major Decisions in the House and Senate Since 1935

Centers for Medicare & Medicaid Services: Trustees Report & Trust Funds

Social Security: The Trust Funds from the Congressional Research Service